Guaranteed life insurance is a viable option for many people to get coverage—however, it isn’t for everyone

In most cases when you apply for a life insurance policy, you will have to fill out an extensive questionnaire, submit your complete medical records, and undergo a medical exam. Based on the results, the insurance company will place you in a risk class and present you with your premium. If you are young, in good health, and do not have a highly risky job, there is a good chance that you will be able to get a relatively low cost monthly insurance premium.

However, this is not the case for many people who are looking for insurance coverage. If you are older or have health complications and need to get life insurance, it can be a lot more difficult to find coverage through the traditional application process. Because getting insured is so important—no matter your health status—there are guaranteed issue life insurance policies. In this article, we’re going to be going over what is a guaranteed issue life insurance policy and what is not, how to apply, and what to expect when you purchase guaranteed issue life insurance.

Guaranteed Issue Life Insurance vs. No Medical Exam Life Insurance

While these types of insurance may sound the same at first, they are actually very different

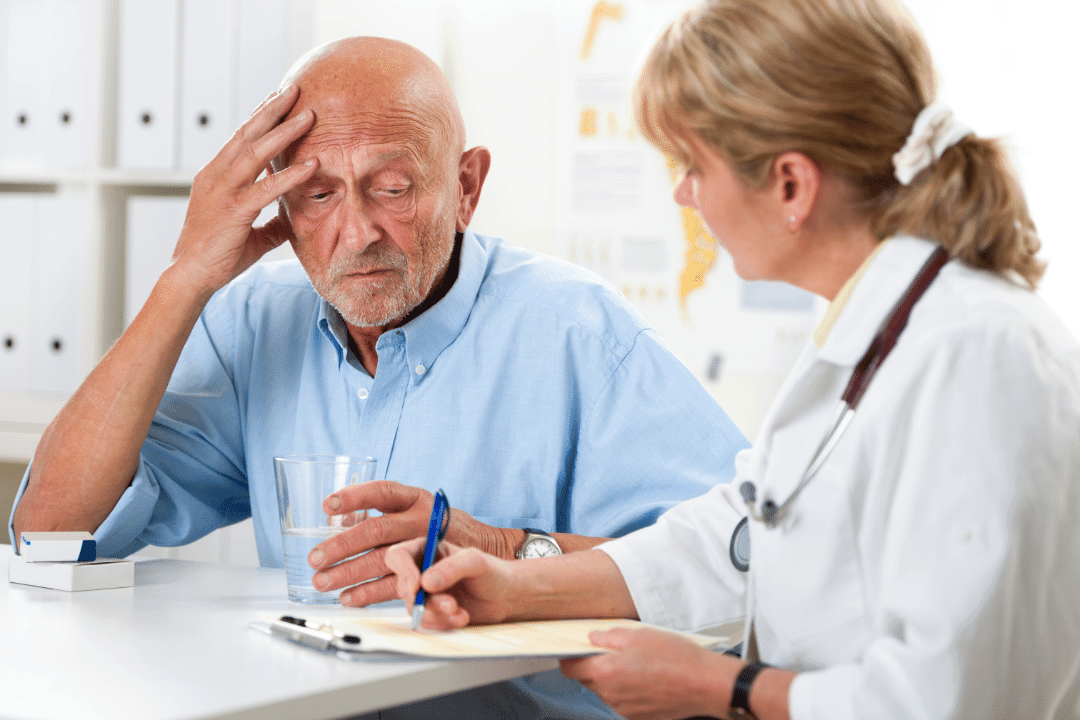

Most life insurance policy types require a medical exam.

One of the main points of confusion about guaranteed life insurance is that it often gets mixed up with no medical exam life insurance. Guaranteed issue life insurance is a type of insurance that is geared toward older individuals—usually over 50 years old. Guaranteed issue life insurance also is usually a low coverage amount and has a required waiting period until the coverage kicks in. Additionally, guaranteed issue life insurance does not require any questionnaire, transfer of records, or a medical exam.

No medical exam life insurance on the other hand is very different. Though you are not required to undergo a medical exam, you are still required to hand over your medical history and fill out an extensive health questionnaire. A no medical exam policy works by cutting out the medical exam step, which allows individuals to get life insurance quickly and without the anxiety of undergoing a medical exam.

While guaranteed life insurance and no medical exam insurance both do not require a medical exam they are designed for different groups of people. Now that we know the difference between these often confused types of life insurance, let’s take a look at how exactly guaranteed issue life insurance works.

How Does Guaranteed Issue Life Insurance Work?

Guaranteed life insurance is designed for specific circumstances. Keep reading to find out guaranteed issue insurance is the right option for you

No one who meets the criteria is denied guaranteed issue life insurance.

If you’re exploring different types of insurance, you have likely encountered the terms “whole life insurance” and “term life insurance.” While a term life insurance is only active for the agreed upon term, whole life insurance never expires. Guaranteed issue life insurance is a type of whole life insurance because it never expires.

One of the unique aspects of a guaranteed life insurance policy is the waiting period. After you have purchased your policy, there is a waiting period—usually anywhere from 2 to 3 years. If you pass away within this waiting period, your surviving family members will not receive the death benefit. However, your family members are not left with nothing either. In the case that you pass during the waiting period, your family members will receive the total cost of the already paid premiums plus interest. In most cases, the interest rate is around 10%.

The waiting period is in place to prevent people from taking out insurance policies in their last days. Unfortunately, without a waiting period, it would be difficult for any insurance company that offers guaranteed policies to stay in business. Now that we know a little bit more about how a guaranteed issue life insurance policy works, let’s find out who stands to benefit the most from this type of policy.

Who is a Good Candidate for Guaranteed Issue Life Insurance?

Getting guaranteed life insurance is only for people with a specific set of circumstances

Guaranteed insurance works for people who receive home care or are in an assisted living facility.

If you are a person who is young and healthy, there is no need to consider getting guaranteed issue life insurance. Guaranteed life insurance is specifically designed for people who would otherwise be unable to get a life insurance policy that offers a death benefit. A death benefit is an important asset to surviving family members to carry out responsibilities that come after death. For example, a death benefit can be used to cover funeral expenses or pay off remaining medical debts. If you are over the age of 50 and have any of the following conditions, then you are probably a good candidate for guaranteed issue life insurance:

- Illness with terminal prognosis

- HIV/AIDS diagnosis

- You are in a nursing home or require regular nursing care

- Cancer diagnosis

- Alzheimers or dementia diagnosis

- You are waiting for an organ transplant

- You require dialysis

- You have a chronic illness that requires you to use a wheelchair

Often, older people who have these types of conditions have a highly variable health status. For other types of insurance policies, this is too much of a risk for the insurance company to take on. If you are older and want to leave behind an insurance policy—but have been rejected over and over—then a guaranteed issue is probably the best avenue for you.

How Much Does Guaranteed Issue Life Insurance Cost?

Guaranteed issue life insurance policies are expensive when compared to the payout amount

Guaranteed life insurance is expensive, but ultimately worth it to provide some coverage.

Just like with any other type of insurance, the cost of your monthly premiums will be dependent on the amount of coverage you purchased. The amount of coverage offered by insurance companies is usually anywhere between $5,000 and $25,000—which is a low amount compared to regular life insurance policies. For this small amount of coverage, you can expect to pay a high premium since the payout is guaranteed after the waiting period and will likely happen within the next few years. Though getting a small amount of coverage for a high price doesn’t sound appealing, for a lot of people this is their only way to get life insurance. Plus, it is always a good idea to leave something behind for your loved ones no matter the amount.

Is it Worthwhile to Apply for other Policy Types?

In most cases, it is a good idea to apply for different types of insurance policies to determine which one is best suited for you

When shopping for insurance policies it is beneficial to consider all of your options.

Too often, people will apply for a guaranteed issue life insurance policy without exploring other options first. If you are over 50 and have health complications, that doesn’t automatically mean that guaranteed issue is the best option. In some cases, if you live long enough, you’ll end up paying the same amount to the insurance company as your death benefit.

Even people who have had a recent heart attack or other types of illnesses can get insurance coverage other than guaranteed issues. Though your premium will likely be high after you are approved, you’ll likely be able to secure a higher coverage amount than with a guaranteed issue. So, if you don’t have one of the conditions we’ve previously listed, getting a different type of policy is probably a better idea. We recommend applying for a few different types of policies to make sure that you are getting the ideal amount of coverage for the best price.

There is never a bad time to search for a life insurance policy. Even if you are older and have health complications, there are still ways to provide for your family after you’re gone. Only you can decide whether or not guaranteed issue life insurance is the best option for you. By doing a little bit of research, you can find the best type of policy that gets you the coverage you need within your budget.